The retail finance market has undergone a complete transformation in India in the last several years. For most buyers, today it is no longer a case of acquiring a brand-new smartphone, laptop, or other consumer durable, but rather of availing of EMI schemes provided at the point of sale or fintech networks that are partners with the company. This transition has made credit accessible to millions of first time borrowers, but on the downside, there is one common issue – a significant majority of customers default on their first EMI. To overcome this, the lender is increasingly relying on device locking as a useful risk management tool.

Understanding First-EMI Defaults

A first-EMI default occurs when a borrower fails to pay even the initial installment after taking a financed device. This is different from a default occurring several months into a loan tenure, because it often signals either weak intent to repay or financial stress that existed before the loan was even disbursed. For lenders, early defaults are particularly damaging. They distort credit risk models, increase collection costs, and erode the margins that thin retail finance products depend on. Smaller NBFCs and digital lenders, who often serve customers with limited credit history, find these early failures especially hard to absorb, since recovery on a single unpaid device rarely covers the cost of the loan itself.

The Role of Automated Device Locking Technology

Automated device locking works through a software that is available to the lender on the financed device, which, using a secure backend system, can limit the device’s functionality if the EMI payment is missed. This may be a gentle lock (remind the user to pay) or a hard lock (only emergency functions available). Upon payment, device will unlock automatically.

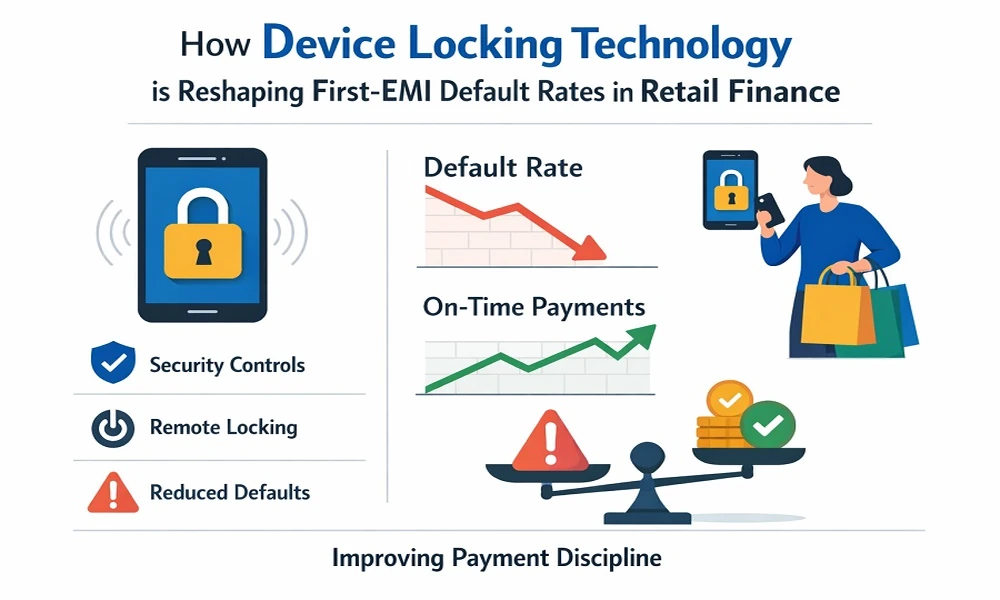

This system provides lenders with a direct approach to control financed assets besides just calling or sending agents to the field. It also changes the mindset of the debt repayment. If a customer realises that if they miss their payment, it will be seen by them, this motivation to pay on time increases significantly. In this context, device locking isn’t simply a punishment for default, it’s a push to not default.

Benefits for Retail Finance Providers

Lenders who have adopted device locking report a noticeable improvement in repayment discipline during the earliest and riskiest stage of the loan cycle. A few specific advantages stand out. Default rates on first installments tend to decline because the consequence of missing payment is immediate and tangible rather than abstract. Communication with borrowers also improves, since locking systems are usually paired with automated reminders and in-app notifications that give customers a chance to act before restrictions kick in. Recovery processes become smoother too, as the lender no longer needs to chase a device that may already be resold or untraceable. Finally, the broader digital lending ecosystem becomes more secure, since this approach reduces reliance on physical repossession, which is costly and often impractical at scale.

Customer Experience and Ethical Considerations

While device locking offers real benefits, it has to be implemented carefully. Borrowers should be informed clearly, at the time of purchase, that the device carries locking functionality tied to repayment. Hidden or poorly disclosed locking mechanisms create distrust and can invite regulatory scrutiny. Responsible lenders pair device locking with grace periods, multiple reminders, and accessible customer support so that genuine cases of delay, rather than intentional default, are not treated harshly. The goal is not to punish customers but to create a fair structure where both the lender’s risk and the borrower’s convenience are respected. Used transparently, device locking becomes less of a threat and more of a built-in nudge toward financial discipline.

Conclusion

Automated device locking technology is proving to be one of the more effective tools available to retail finance companies trying to control first-EMI default rates. It addresses the problem at its root, the earliest and most vulnerable stage of the repayment cycle, while giving lenders better visibility and control over financed assets. As India’s digital lending sector matures, technologies like device locking, when deployed transparently and ethically, are likely to become a standard part of responsible lending infrastructure rather than an exception.